Unless you have very long AR and AP payment terms, and very long wip cycles, then I don't see much point in revaluing P&L that way (though it is commonly done). However, you always have to consider the tax regime.

What do the accounting standards say - in general they don't support the use of average rates! (The use of an average rate is generally acceptable where transactions occur uniformly throughout the year.) The other reason for average is when the historical daily rate is not known. For FASB 52 compliance, balance sheet accounts with foreign currency postings (e.g., open payables/receivables) must be revaluated to the Local Currency using the exchange rate in affect as of the balance sheet date. Revaluation is normally run on a period-end basis as part of month-end close using at a minimum an average exchange rate method (spot rates are the preferred method). P&L Accounts in a foreign currency, represented by revenues, expenses, Gains/Losses will use the spot exchange rate on the date those postings were recognized. If a spot rate is not available the n an average rate would be used. So I agree with Ludwig that daily rate update is preferable.

If at all possible, use the spot rate when calculating the balance sheet and P&L account currency revaluation (Gain/Loss postings and currency translation from Functional Currency to Group Currency). Adjustments posted to CTA should be recorded similarly. SAP has many transaction codes that allow for updating the foreign currency exchange rates; OC41 is one of them.

IAS 21 The Effects of Changes in Foreign Exchange Rates prescribes:

- How to include foreign currency transactions and foreign operations in the financial statements of an entity; and

- How to translate financial statements into a presentation currency.

IAS 21 answers 2 basic questions:

- What exchange rates shall we use?

- Functional vs. Presentation Currency

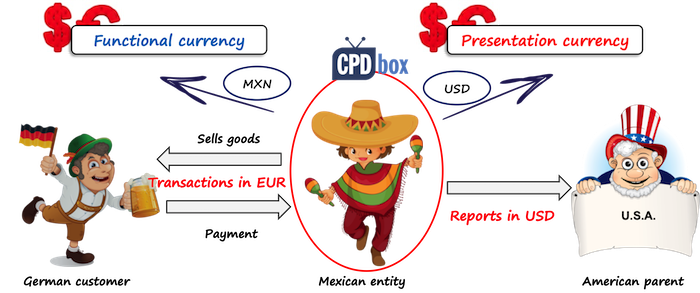

IAS 21 defines both functional and presentation currency and it’s crucial to understand the difference:

Functional currency is the currency of the primary economic environment in which the entity operates. It is the own entity’s currency and all other currencies are “foreign currencies”.

Presentation currency is the currency in which the financial statements are presented.

In many cases, functional and presentation currencies are the same.

An entity can decide to present its financial statements in a currency different from its functional currency – for example, when preparing consolidation reporting package for its parent in a foreign country.

While an entity has only 1 functional currency, it can have 1 or more presentation currencies, for its financial statements

An entity can actually choose its presentation currency, but it CANNOT choose its functional currency.

The primary economic environment is the one in which the entity primarily generates and expends the cash.

Sometimes, sales prices, labor and material costs and other items might be denominated in various currencies and therefore, the functional currency is not obvious and management must use its judgment to determine the functional currency that most faithfully represents the economic effects of the underlying transactions, events and conditions.

Initially, all foreign currency transactions shall be translated to functional currency by applying the spot exchange rate between the functional currency and the foreign currency at the date of the transaction.The date of transaction is the date when the conditions for the initial recognition of an asset or liability are met in line with IFRS. Subsequently, at the end of each reporting period, you should translate:

- All monetary items in foreign currency using the closing rate;

- All non-monetary items measured in terms of historical cost using the exchange rate at the date of transaction (historical rate);

- All non-monetary items measured at fair value using the exchange rate at the date when the fair value was measured.

All exchange rate differences shall be recognized in profit or loss, with the following exceptions:

- Exchange rate gains or losses on non-monetary items are recognized consistently with the recognition of gains or losses on an item itself.

For example, when an item is revalued with the changes recognized in other comprehensive income, then also exchange rate component of that gain or loss is recognized in OCI, too.

- Exchange rate gain or loss on a monetary item that forms a part of a reporting entity’s net investment in a foreign operationshall be recognized:

- In the separate entity’s or foreign operation’s financial statements: in profit or loss;

- In the consolidated financial statements: initially in other comprehensive income and subsequently, on disposal of net investment in the foreign operation, they shall be reclassified to profit or loss.

When there is a change in a functional currency, then the entity applies the translation procedures related to the new functional currency prospectively from the date of the change.

When an entity presents its financial in the presentation currency different from its functional currency, then the rules depend on whether the entity operates in a non-hyperinflationary economy or not.

When an entity’s functional currency is NOT the currency of a hyperinflationary economy, then an entity should translate:

- All assets and liabilities for each statement of financial position presented (including comparatives) using the closing rate at the date of that statement of financial position.

Here, this rule applies for goodwill and fair value adjustments, too.

- All income and expenses and other comprehensive income items (including comparatives) using the exchange rates at the date of transactions.

Standard IAS 21 permits using some period average rates for the practical reasons, but if the exchange rates fluctuate a lot during the reporting period, then the use of averages is not appropriate.

All resulting exchange differences shall be recognized in other comprehensive income as a separate component of equity.

However, when an entity disposes the foreign operation, then the cumulative amount of exchange differences relating to that foreign operation shall be reclassified from equity to profit or loss when the gain or loss on disposal is recognized.

When an entity’s functional currency IS the currency of a hyperinflationary economy, then the approach slightly changes:

- The entity’s current year’s financial statements are restated first, as required by IAS 29 Financial Reporting in Hyperinflationary Economies. Comparative figures are used the same as current year’s figures in the financial statements from previous reporting period.

- Only then, the same procedures as described above are applied

![]()

So that is why erp systems generally don't calculate an average rate.

https://www.iasplus.com/en/standards/ias/ias21